AI Driving Vocational Higher Ed Enrollments

Case Study of Lincoln Educational Services (LINC) and What is Driving the Stock Price

A former colleague recently asked me to take a look at Lincoln Educational Services (NASDAQ: LINC) after noticing that the stock had appreciated by more than 100% over the past year.

For those of you who are Gen X or older, you probably remember the old Lincoln Technical Institute advertisements (“if you’re unemployed or underemployed”).

For most of its history as a public company, Lincoln was never one of the larger publicly traded for-profit education operators relative to its peers. Throughout much of the 2010s the company’s market capitalization remained below $500 million. Investors viewed it as a niche vocational training provider.

That makes the company’s current position somewhat surprising.

Lincoln now has a market valuation of over $1B. In fact, its market capitalization now exceeds that of Phoenix Education Partners (PXED), the owner of the University of Phoenix (disclosure: I own the stock). Having covered the sector for many years, that is not an outcome I would have predicted.

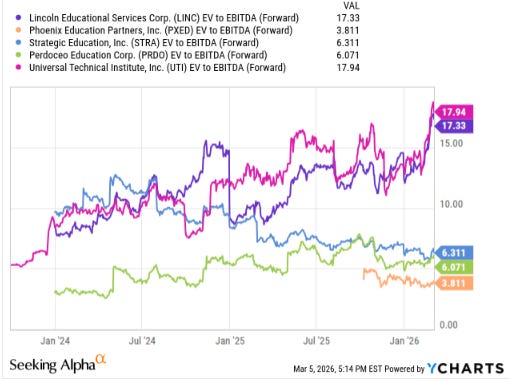

The comparison is striking when looking at the underlying financials.

Phoenix Education generated nearly $1B in revenue over the past twelve months with a 19% operating margin. Lincoln, by comparison, generated roughly half that revenue — $518 million — with an operating margin of about 6% over the same period.

Yet despite producing far less revenue and significantly lower margins, Lincoln is currently valued more highly by the market.

Two factors explain this divergence.

Revenue growth. LINC in its most recent fiscal year ending Dec 2025 saw an 18% YoY revenue growth rate. PXED in comparison only grew by 6% in their last fiscal year ending August.

Valuation multiple. The market is ascribing a 17x EV/EBITDA multiple whereas PXED has only close to a 4x EV/EBITDA multiple.

This multiple gap is not unique to Phoenix. The same pattern appears across the publicly traded education sector. The vocational training providers — Lincoln Educational Services and Universal Technical Institute — trade at significantly higher valuation multiples than regionally accredited university operators such as Strategic Education (owner of Capella and Strayer University), Perdoceo (owner of American Intercontinental University and Colorado Technical University), and Phoenix Education Partners.

An interesting shift occurred beginning in early 2025. Historically, Strategic Education historically traded at the highest valuation multiple within the group because investors viewed it as the highest quality operator. That relationship has now changed.

Since January 2025, Lincoln’s valuation multiple has expanded dramatically — nearly doubling — while Strategic Education’s multiple has compressed. The result is the striking divergence in valuation multiples visible in the chart above.

The obvious question: what changed?

Part of the explanation is growth. The vocational operators are growing revenue faster than their degree-granting peers.

Lincoln Educational Services and Universal Technical Institute are generating double-digit revenue growth, driven by rising student starts and the opening of new campuses tied to skilled-trade programs such as automotive technology, HVAC, welding, and electrical systems. Demand for these programs appears strong because employers continue to face persistent shortages of technicians in these fields.

By contrast, the traditional for-profit university operators are largely mature businesses. Strategic Education, Perdoceo, and Phoenix Education Partners are generally reporting low- to mid-single-digit organic revenue growth at best. These institutions are not expanding their campus footprints in the same way as they don’t have physical campuses. Their enrollment growth is constrained by competition from nonprofit universities and state institutions that increasingly offer similar programs online at comparable or lower prices. For-profit institutions historically filled this gap because traditional universities were slow to adapt to what working students needed: flexibility, online delivery, and customer support.

The vocational providers are expanding capacity to meet labor demand in skilled trades. The degree granting institutions operate in a much more competitive market.

That difference in growth trajectory explains why the market is assigning a much higher valuation multiple to LINC and UTI than to the traditional for-profit university operators.

This divergence also reflects something more meaningful than simply revenue growth rates. There is a case to be made that there is a broader issue at play, namely how investors are thinking about the future of work in an economy increasingly shaped by artificial intelligence.

Yes, I realize you’ve read elsewhere about how AI will automate white-collar labor. Research, coding, financial modeling, marketing content, customer support, legal analysis — these are all areas where software is already beginning to substitute for human labor. Over the next decade we will see how much knowledge work can realistically be performed by machines.

We all know where this leads.

Meanwhile, repairing an HVAC system, diagnosing a vehicle problem, installing electrical infrastructure, or welding structural components still requires hands-on problem solving in the physical world rather than the digital one. Perhaps Tesla will eventually build Optimus robots capable of performing these tasks, but that scenario seems unlikely within the next ten years.

Demographics are also working in favor of the trades. Much of the existing skilled-trade workforce is approaching retirement age, while the pipeline of younger workers entering these fields has been thin for decades.

There may also be broader cultural forces at work. For decades, American society steered students toward four-year degrees while treating trade work as second class. The result:

Anthropology/Sociology/English majors with purple hair and nose rings protesting global politics

Not enough people who know how to repair a transmission or install an HVAC system.

This phenomenon has started to enter the culture. See the South Park episode Joining the Panderverse from 2023. In that episode, the show makes a running joke about how no one knows how to do skilled trades anymore. Had investors purchased LINC stock after watching that episode, they would have seen a 3x return on their investment.

Regardless of how artificial intelligence reshapes the digital economy, one thing is certain: the physical economy will still require human labor.

Electric vehicles will need technicians capable of repairing complex drivetrains and battery systems. Data centers will require electrical and cooling systems maintained by skilled technicians. Buildings still need HVAC installation and maintenance, and industrial facilities continue to rely on welders and electricians.

Meanwhile, MBAs and other white-collar credentials — whether issued by traditional universities or for-profit institutions — are increasingly commoditized.

The valuations of publicly traded education companies appear to reflect this reality. The market seems skeptical that traditional degrees will generate strong long-term demand growth.

Vocational providers such as Lincoln and UTI, on the other hand, are valued as mission critical infrastructure providers for the skilled labor economy.

If investors are correct, the story behind Lincoln’s stock is a signal of the new reality of our post-AI world.

The market is pricing a world where the most valuable education is not the one that teaches you how to analyze spreadsheets (Claude can apparently do that for you) — but the one that teaches you how to fix the machines that run them.

Appendix: The “Meat and Potatoes” Explanation for Why the Stock Went Up

In the main article I use Lincoln as a lens to talk about broader themes such as AI and the future of work. For readers who prefer a more straightforward explanation of why the stock actually moved, the answer is simpler.

Lincoln’s valuation multiple expanded because the company delivered beat and raise quarters throughout the year. When companies repeatedly exceed expectations and raise guidance, analyst estimates move higher throughout the year. Rising earnings estimates lead to higher valuation multiples.

Lincoln’s Original 2025 Guidance

When Lincoln reported its 2024 results, management guided to the following for 2025:

Revenue: $480M–$490M

Adjusted EBITDA: $55M–$60M

Student starts growth: 8%–12%

Lincoln’s 2025 Results

When Lincoln reported full-year 2025 results management reported financial results well above the original guidance:

Revenue: $518.2M

Adjusted EBITDA: $67.1M

Student starts: 15.2% (excluding transitional segment)

The stock’s move was a result of quarterly guidance increases.

Was management as surprised as investors regarding better than expected results? Did they sandbag guidance? Don’t know.

Rising estimates combined with improving fundamentals is how sustained stock price moves are created.

Its conceivable that LINC financials miss and the stock plummets. Don’t take this write-up as investment advice.

Disclaimer / Disclosure

The author beneficially owns shares of Phoenix Education Partners (PXED). As a result, the author has a financial interest in the performance of that security and readers should consider this potential conflict of interest when evaluating the analysis and conclusions presented herein.

This document reflects the author’s personal views and opinions as of the date of publication and is subject to change without notice. The information contained herein has been obtained from publicly available sources believed to be reliable; however, the author makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information.

This material is provided solely for informational and educational purposes and does not constitute investment advice, legal advice, accounting advice, or tax advice. Nothing herein constitutes an offer to sell, a solicitation of an offer to buy, or a recommendation regarding any securities transaction. Any forward-looking statements are inherently subject to risks, uncertainties, and assumptions, and actual results may differ materially.

Investors should conduct their own independent due diligence and consult their financial, legal, and tax advisors before making any investment decisions.

It’s that markets may be repricing scarcity.

Digital skills scale with software. Once automation reaches a certain threshold, the supply of that capability effectively explodes. Physical skills move in the opposite direction. Training takes years, certification takes time, and the work itself cannot be virtualized.

So you end up with a reversal of the last few decades.

For a long time the premium went to abstract knowledge work. If AI compresses that advantage, the relative value of skilled trades may rise simply because they remain tied to the physical world.

Markets may just be adjusting to that constraint earlier than the education system has.

Great article. Not the type I read (I do work at the intersection of AI & education) and that's precisely why I loved it.